Banks in the loan or mortgage business believe they know their clients well, yet they struggle to offer services that capitalize on customer data or tailor the loan origination experience to the individual based on the existing volume of information they have.

That’s one of the key takeaways from Mortgages: A Digital Process to Be Mastered, a new report from MongoDB and FinTechFutures. The report, which surveyed 104 retail banking, business banking, and corporate banking executives, highlights that customer pain is particularly acute when — despite collecting reams of information about clients — banks and loan originators are still unable to turn around loan requests in a timely manner or offer personalized experiences.

Click here to check out the Panel Discussion.

Do You Really Know Your Customer?

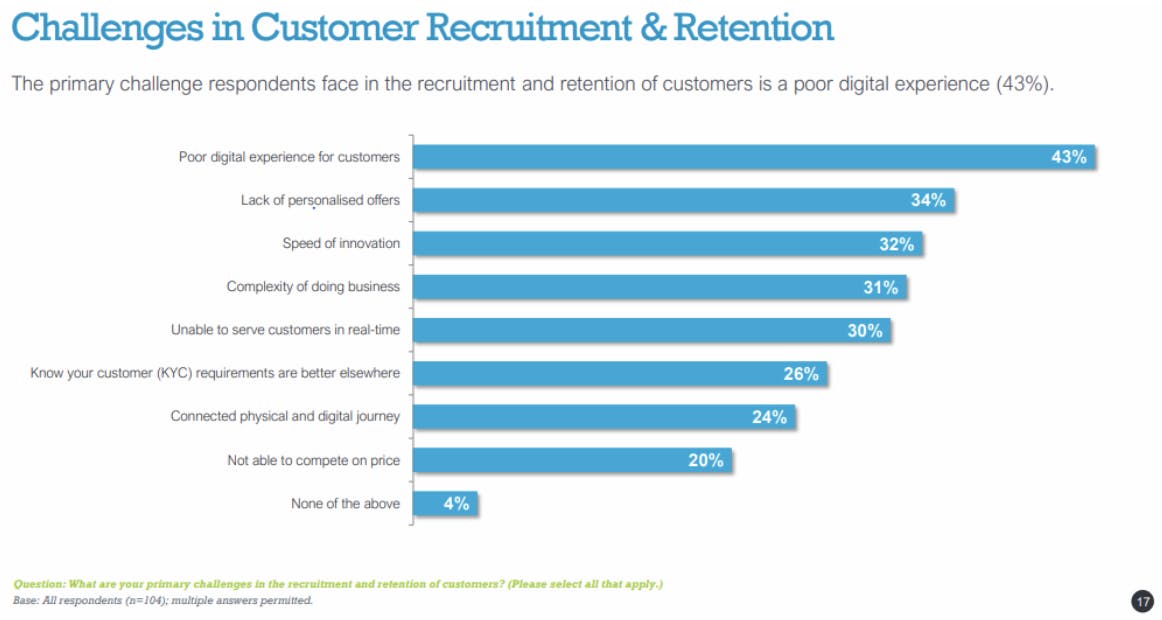

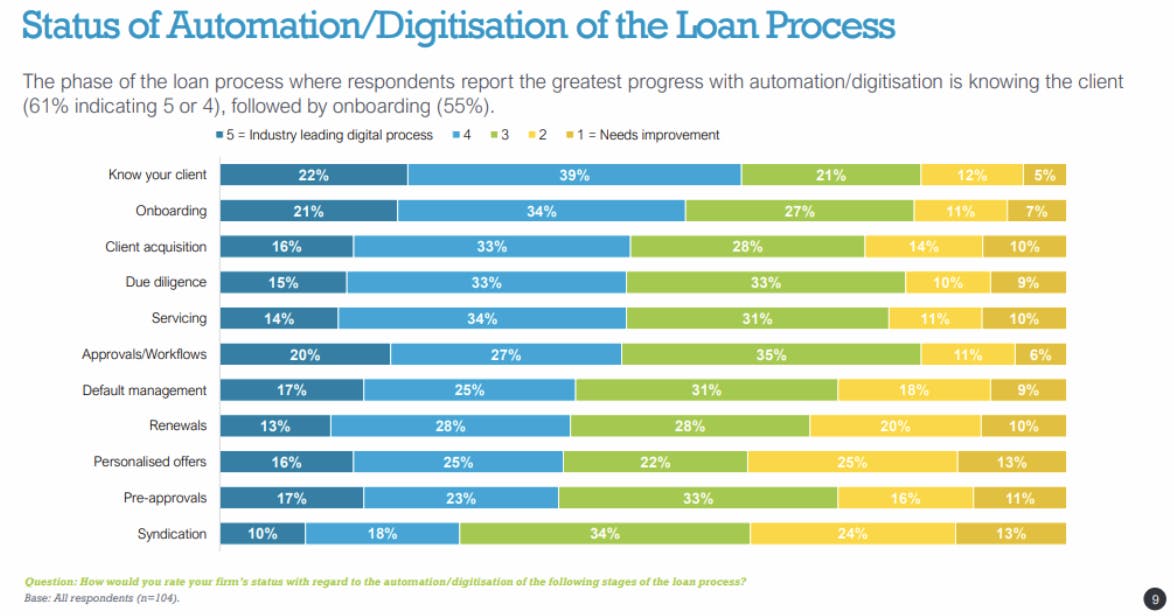

According to the report, 61% of financial executives said they have industry-leading Know Your Client (KYC) processes. But at the same time, 43% also named poor digital experiences as a barrier to recruiting and retaining customers, with the inability to deliver personalized offers coming in second at 34%. Other issues commonly cited include the speed of innovation, the complexity of doing business, and the inability to serve customers in real time. So, do banks really know their customers? And if they do, what are they doing with that information if not using it to better serve their customers?

What’s holding the industry back? Outdated processes, with agents and employees forced to grapple with manual processes, shuffling paper piles, and creating spreadsheets before they can get to work serving the customer. The market is crying out for better automated and data-driven decisions, and legacy systems can’t keep up.

Besides the obvious waste of people resources, the lack of a holistic digital offering also hurts business. Customers increasingly cite easy to use and transparent mortgage processes, smooth onboarding, and digital processes as factors behind the lender they choose.

Behind the Numbers

Banks have made some progress digitizing and automating what were once almost exclusively paper-based, manual processes. But the primary driver of this transformation has been compliance with local regulations rather than an overarching strategy for really getting to know the client and achieving true customer delight.

It’s a missed opportunity for a couple of reasons. First, banks create a comprehensive client profile during the onboarding process. They have enough data to perform risk assessments and personalize offers, but instead default to “new client onboarding” processes that are 30+ years old. The simple fact that the consumer is already a long term client with detailed information is ignored. The famous example is the ask for pay slips while the bank can see the actual monthly (or weekly) pay moving in to begin with.

Second, most bank customers stay with their chosen financial institution for their entire lifetimes. And as the client relationship matures, the insight banks can bring to bear become deeper and richer. But a slow approval process (40%) and slow response times (39%) were two of the top areas in need of improvement cited in the survey. These are not the hallmarks of industry-leading KYC processes or deep client relationships, but of siloed data and misalignment of digital strategy.

What we’re seeing is the difference between the practice of ensuring compliance with local regulations and a strategic imperative for truly understanding the client. While modernization investments have helped automate much of the paper-pushing related to compliance, transforming customer experiences and making LOS more transparent have yet to be achieved.

Most executives in the survey planned on leveraging real-time analytics, AI/ML, and workflow software to improve processes. These are all technologies that can take KYC processes beyond simple compliance use cases and lead to more value-added, personalised client relationships.

Smart Money

Today’s clients are demanding fully modern, mobile-first banking experiences.

To meet those expectations, bank executives and IT leaders plan to invest in technologies that can address some of their most glaring needs. Chief among them include getting away from manual processes like email and spreadsheets, better data analytics for decision making, and gaining access to real-time information at every touchpoint in the customer journey.

The investments they’re willing to make include real-time analytics, artificial intelligence, and machine learning (AI/ML). Along with digital customer experiences (for example, chatbots and personalized recommendations), these are the three areas that bank executives and IT leaders say will drive greater market share and profitability in the loans business.

So, even though many banks have started the journey toward modernization, they still have further to go before they’re able to meet the expectations of their clients. It’s not about reducing the paper-pushing or satisfying regulatory requirements involved with the LOS business. It’s about personalization and real-time experiences, hallmarks of true KYC.

Mortgages are a Digital Process to be Mastered

If real-time data and AI/ML are the way forward for driving value and transforming customer experiences, it will have to be accompanied by modernization of the underlying data architecture.

As bank executives and IT leaders in the survey acknowledge, the lack of a digitization strategy, speed to market, and costly legacy migration are their top three concerns when digitizing their mortgage processes. A de-siloing of data and the introduction of data mesh concepts allows the leap from modernizing legacy infrastructure to digital transformation and competitive advantages.

Banking innovators strive to be first to market, but legacy systems are holding them back, stymying digitization strategies. Overcoming these and other challenges requires the introduction of a modern data domain model that integrates the transactional and process workloads and augments customer data with information from other legacy and external systems.

MongoDB Atlas is perfectly suited for this purpose. We have deep experience building customer 360 models that can be mapped to omnichannel interactions.

In addition, MongoDB also has proven capabilities integrating risk and treasury functions (for mortgages this means funds transfer pricing and credit risk), with MongoDB Atlas being used by many banks and other financial service providers in the mortgage space, from building societies in the UK to special purpose lenders in Australia.

Lastly, MongoDB’s ability to integrate mobile experiences, search capabilities, and real-time analytics (for example, scoring for consumer ratings while that consumer is on a web page) makes MongoDB the proven data platform for mortgage modernization and true digital transformation.